By: Jay Whitney

Seller’s Discretionary Earnings (SDE) is the total financial benefit that a single full-time owner operator would derive from a small business on an annual basis. It is also referred to as Seller’s Discretionary Cash Flow, Adjusted Cash Flow, Owner Benefit, or Recast Earnings. SDE includes all cash flows to an owner including adjustments for owner’s salary, discretionary expenses, and nonrecurring income/expenses.

Below is the step-by-step details of how to calculate SDE for a typical single location childcare center business.

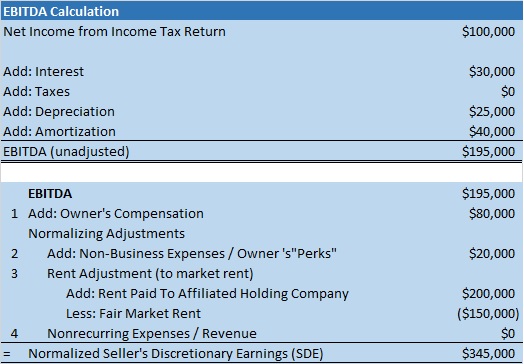

The Earnings Before Interest Taxes Depreciation and Amortization (EBITDA) calculation is shown below:

To calculate the SDE, adjustments need to be made as follows:

- Owner’s Compensation is included in the Compensation of Officers (line 7 in the S Corp tax return). The owner’s W-2 is needed for a business valuation to assure that the Compensation of Officers just includes the owner’s compensation as an add-back. This is because this line item may also be non-owner officer’s compensation. Furthermore, if there is more than one owner (or family member) who works, their wages must be replaced with fair market replacement wages, since the SDE earnings stream is for a single owner-operator. A common example of this is if the owner’s spouse does not receive a paycheck, but does repairs/maintenance on the weekends and evenings, then an adjustments for the estimated cost of having a person preform these tasks currently done by the spouse must be made. Employer portion of payroll taxes paid based on the W2 salary of one owner is also included as an adjustment to SDE.

If the valuation is on a single location center that is owned by an absentee owner, the manager’s/director’s salary should be adjusted to reflect as if the center was an owner operated childcare business.

- Owner’s Perks/Non-Business expenses include expenses paid for by the childcare center that benefit the owner (owner’s health insurance premium, owners retirement contribution, payroll taxes on owner’s salary, owner’s personal auto, salary paid to non-working family members, etc.). Non-Recurring expenses include expenses like one-time gains or losses on asset disposal, broker fees, major repairs to the roof or HVAC equipment, and other unusual items.

- Fair Market Rent – The owners of many childcare center businesses also own (through a holding company or individually) the real estate used by the business. In this case, rent the business pays above or below market must be adjusted to reflect the fair market rent a hypothetical buyer of the business would pay to an unrelated landlord. Sometimes, a childcare center business doesn’t pay any rent because it owns the real estate on which it operates, in which case, a fair market rent expense must be added.

When making a fair-market rent adjustment, any expenses (property tax, insurance, and repairs/maintenance) paid for by a holding company must be considered.

In the table above, yearly fair market rent was estimated at $150,000.

- Nonrecurring Expenses / Revenue adjustments would include extraordinary items like if the childcare center had recently lost the CACFP food program, or some other major state support which will not likely be regained for an extended time. A child abuse situation occurring in a center where a substantial number of children left would be another example.

All adjustments must be documented. It is better to be conservative in your estimates than aggressive.

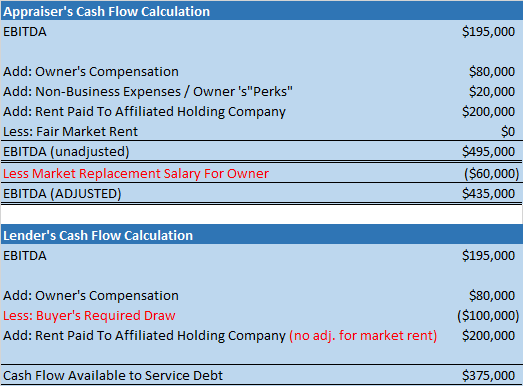

“Cash Flow” can be significantly different to different people. Lenders make adjustments to the cash flow that are specific to the deal terms and borrower’s draw requirements. Business valuation appraisers don’t consider these above items, and instead base the valuation on a hypothetical transaction which assumes one owner-operator for the childcare business. See below:

Business valuations generally use the SDE when valuing a single location childcare center that is managed by the owner. Adjusted EBITDA is used to value multiple childcare centers that are absentee owned and managed by a general manger over all childcare centers. Because most single location childcare centers are typically owner operated, the Adjusted EBITDA may not be used in a business valuation.

Of note is that the Lender’s Cash Flow Available to Service Debt is the amount to service the debt of the combined childcare business and real estate.

Buyer may sometimes make adjustments to the cash flow for “Owner Perks” that neither the Appraiser nor Lender will use. Examples of Owner Perks that only a Buyer may use are:

- Multiple dinner restaurant bills charged to the business where the Owner and her spouse discussed the business.

- The travel expense charged to the business for a Board of Directors meeting in Hawaii.

- Expenses to buy furniture for the owner’s home office.

The above examples are all valid business expenses that most likely would not have been incurred by the business unless they benefited the business owner in some way, however, appraisers and lenders will generally not use them in calculating “Cash Flow”. Unless these expenses have very detailed documentation and are verifiable, most buyers will not use them either.

Examples of expenses that would NOT qualify as adjustments would include:

- Any marketing or promotion related expense even if it “didn’t work and it wouldn’t be done again”

- Counting unreported cash sales unless the buyer has a straightforward means to verify such sales

- Counting dozens of personal purchases on a credit card where the card is also used for business purchases, or where the expenses are buried in a much larger expense category or several expense categories and therefore nearly impossible for a buyer to verify.

When a childcare owner owns several centers and is just selling one of the centers, there is a great opportunity for a seller to shift sales and expenses between businesses. Sellers should expect a buyer to want to use a financial advisor who also understands the childcare center business to check over the seller’s books at more than just the one location.

Contact us to discuss childcare valuations, or request a valuation.

JayWhitney@ChildcareBrokers.com 770-410-7582